In today’s workplace, employee financial wellness is no longer a...

How Instant Approval Loans & Same-Day Loan Disbursement Work?

Instant approval loans are designed for speed and convenience, providing quick access to cash when you need it most. However, understanding the mechanics of how these loans work is crucial to making informed decisions and avoiding potential pitfalls. In this section, we’ll break down the entire process, from application to disbursement, and explore what you need to know to navigate the world of instant approval loans effectively.

The Application Process

Applying for an instant approval loan is generally straightforward, but it’s essential to be prepared and understand each step involved. Here’s a typical overview of how the application process works:

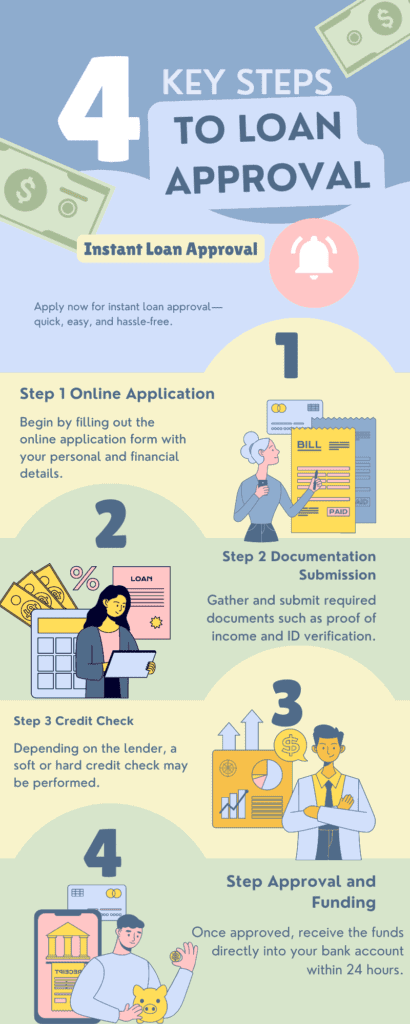

Online Application

Most instant approval loans are applied online, which adds to their convenience and speed. The online application process is designed to be quick and user-friendly, often taking just a few minutes to complete.

- Personal Information: You must provide basic personal information, including your name, address, and contact details. Some lenders may also require you to verify your identity by providing a government-issued ID.

- Financial Information: You’ll be asked to submit details about your income, employment status, and banking information. This helps the lender assess your ability to repay the loan. Be prepared to provide recent pay stubs or bank statements if requested.

Documentation

While some loans, particularly those marketed as “no credit check” loans, require minimal documentation, others might need more thorough verification. It’s essential to gather and prepare the necessary documents to avoid delays.

- Proof of Income: Lenders typically require proof of a steady income to ensure you can repay the loan. This can be in the form of pay stubs, bank statements, or a letter from your employer.

- Bank Account Information: Since most lenders deposit the loan directly into your account, you must provide your bank account and routing numbers. This information is also used for automatic repayments, where applicable.

- ID Verification: To prevent fraud, lenders often require a government-issued ID, such as a driver’s license or passport, to confirm your identity.

Credit Check

One of the most significant aspects of the instant loan process is the credit check, or lack thereof, depending on the loan type.

- Soft Credit Check: Some lenders perform a soft credit check as part of the application process. This inquiry does not affect your credit score but gives the lender insight into your credit history.

- Hard Credit Check: Other lenders may conduct a hard credit check, which can temporarily lower your credit score. This type of check is more thorough and may be required for more significant loan amounts or unsecured personal loans.

- No Credit Check Loans: As the name suggests, no credit check loans do not involve a review of your credit history. These loans are accessible to individuals with poor credit but often come with higher interest rates and fees to compensate for the increased risk to the lender.

How Lenders Assess Your Application

Once you’ve submitted your application and documentation, the lender will assess your eligibility. This process can vary depending on the lender and the type of loan but generally includes the following steps:

- Income Verification

- Lenders need to ensure that you have the means to repay the loan. Your income level and employment status are critical factors in this assessment. Some lenders might approve your application based on a minimum income threshold, while others may look at your overall financial situation, including existing debts.

- Debt-to-Income Ratio

- Your debt-to-income ratio (DTI) is a critical metric that lenders use to determine how much of your income goes toward paying existing debts. A lower DTI ratio indicates you have more disposable income to cover new debt, making you a more attractive candidate for an instant approval loan.

- Employment Status

- Stable employment can significantly increase your chances of loan approval. Lenders typically prefer applicants who have been with the same employer for a reasonable amount of time, which suggests financial stability and reliability.

- Other Factors

- Depending on the lender, other factors such as your residence stability (how long you’ve lived at your current address), the type of bank account you have, and your payment history with other lenders might also come into play.

Typical Timelines for Approval and Fund Disbursement

One of the key selling points of instant approval loans is the speed with which you can receive your funds. Here’s what you can generally expect in terms of timelines

- Application Submission:

- After completing your online application, you can typically expect a response within minutes. The speed of this response is often due to automated systems that quickly assess your eligibility based on the information you provided.

- Approval Notification:

- If your application is approved, you’ll receive an immediate notification. This approval can sometimes be conditional, requiring you to submit additional documents or verify information before the final approval is granted.

- Fund Disbursement:

- Once your loan is fully approved, the funds are usually deposited into your bank account. For many lenders, this happens within 24 hours, although some might disburse the funds on the same day, depending on the time of your application and the lender’s processing speed.

- Exceptions and Delays:

- While most instant approval loans are processed quickly, there can be exceptions. Delays might occur if the lender needs additional information from you or if there are issues with verifying your documentation. To avoid delays, ensure that all your information is accurate and complete.

Understanding the Costs: Interest Rates and Fees

While the speed of instant approval loans is a significant advantage, it’s also essential to understand the costs associated with these loans. High interest rates and fees are standard, especially with payday and no-credit-check loans.

- Interest Rates:

- Instant approval loans often come with higher interest rates compared to traditional loans. This is due to the increased risk lenders take by offering quick loans with minimal verification. It’s not uncommon to see annual percentage rates (APRs) in the triple digits for payday loans.

- Origination Fees:

- Some lenders charge an origination fee, a percentage of the loan amount deducted from the disbursed funds. Be sure to ask the lender if this fee applies to your loan and how much it will be.

- Late Payment Fees:

- Pay a payment or be on time to avoid hefty fees. Ensure you understand the lender’s late payment policy before accepting the loan terms.

- Prepayment Penalties:

- Although less common, some lenders may charge a fee if you pay off your loan early. This is something to watch out for if you can repay the loan beforehand.

Making an Informed Decision

They understand how instant approval loans work, which is the first step in making an informed decision. While these loans can provide quick relief in an emergency, they come with high costs and risks that should be noticed.

Before applying:

Consider your financial situation carefully. Ensure that you can meet the repayment terms without jeopardizing your financial stability.

If you need help determining whether an instant approval loan is the right choice, take the time to explore other options or seek advice from a financial professional.

In the next section, we’ll explore the benefits and risks of instant approval loans in greater detail, helping you weigh the pros and cons to determine if this type of loan aligns with your financial needs and goals.

Instant Approval Loans: Pros, Cons, and No Credit Check Options Explained

Instant approval loans can be a quick and convenient solution when you need immediate funds, but like any financial product, they have advantages and disadvantages. Understanding the benefits and risks of these loans is crucial in making an informed decision that aligns with your financial situation and goals. This section will investigate instant approval loans’ positive and potential pitfalls.

Instant Cash Access with Approval Loans

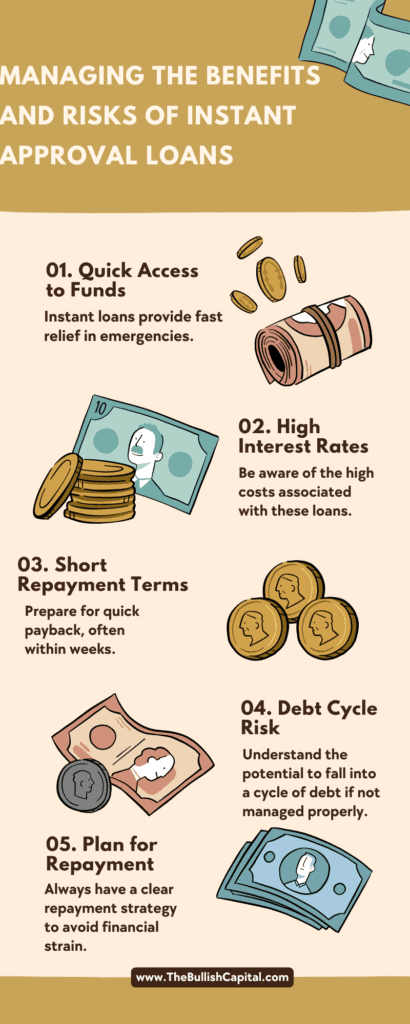

One of the most significant benefits of instant approval loans is their speed. When an unexpected expense arises, waiting days or weeks for a traditional loan approval isn’t only an option for some people. Instant approval loans provide quick access to cash—often within hours of application. This makes them particularly useful in emergencies, such as urgent medical expenses, car repairs, or needing to cover essential bills before your next paycheck.

Simple and Convenient Application Process

Applying for an instant approval loan is much simpler and more convenient than a traditional loan. Most lenders offer online applications that can be completed in minutes. You don’t need to visit a bank or fill out lengthy paperwork. The process is streamlined to provide a quick decision, ideal for those who need money fast and don’t want to deal with the hassle of traditional lending procedures.

No Credit Check Options

Obtaining a traditional loan can be challenging for individuals with poor credit or no credit history. Many instant approval loans, especially payday loans, offer no credit check options. This means that your credit score will be acceptable with the approval process. While this can benefit those who have struggled with credit issues in the past, it’s important to note that no-credit-check loans often come with higher interest rates to compensate for the increased risk to the lender.

Flexible Loan Amounts

Instant approval loans can offer flexibility in the amount you borrow. Whether you need a small loan to cover a minor expense or a more considerable sum for a more significant financial need, options are available to suit different requirements. This flexibility makes instant approval loans accessible to various borrowers with varying financial needs.

No Collateral Required

Most instant approval loans, particularly payday and personal loans, are unsecured. This means you don’t need to put up any collateral, such as your home or car, to secure the loan. This is a significant advantage for borrowers who don’t have valuable assets to pledge or don’t want to avoid losing their property.

Risks of Instant Approval Loans

High Interest Rates

One of the most notable downsides of instant approval loans is the high interest rates that often accompany them. Lenders charge these rates to offset the risk of lending to individuals with poor credit or who need money quickly. While the convenience of fast cash is appealing, it comes at a cost. For example, payday loans can have annual percentage rates (APRs) that reach 400% or more. This makes instant approval loans an expensive option, especially if you need help to repay the loan quickly.

Short Repayment Terms

Another risk associated with instant approval loans is the short repayment period. Many of these loans, particularly payday loans, are designed to be repaid in full within a short timeframe, often within two weeks to a month. This short repayment period can lead to difficulties in repaying the loan on time for borrowers already struggling financially. Failure to repay can result in additional fees, increased interest rates, and the possibility of falling into a cycle of debt.

Potential for a Debt Cycle

The combination of high interest rates and short repayment terms can lead to what’s known as a debt cycle. If you cannot repay the loan by the due date, you might be tempted to take out another loan to cover the first one, leading to a cycle of borrowing that can be difficult to break. This debt cycle can have severe financial consequences, including worsening credit scores, increased debt, and economic stress.

Fees and Penalties

In addition to high interest rates, instant approval loans often come with various fees and penalties that can significantly increase the cost of borrowing. These can include origination fees, late payment fees, and prepayment penalties. Origination fees are typically a percentage of the loan amount and are charged upfront, while late payment fees are incurred if you miss a payment deadline. Though less common, prepayment penalties may apply if you pay off your loan early, depriving the lender of anticipated interest earnings. It’s crucial to fully understand the fee structure of any loan before committing.

Impact on Credit Score

While some instant approval loans don’t require a credit check, others do, which can impact your credit score. For instance, a hard credit inquiry made during the application process can temporarily lower your credit score. Additionally, if you fail to repay the loan on time or default, this can be reported to credit bureaus, further damaging your credit score and making it more challenging to obtain credit in the future.

Predatory Lending Practices

Unfortunately, instant approval loans’ quick and easy nature can make them a target for predatory lenders. These lenders exploit borrowers in desperate financial situations by offering loans with unfair terms, exorbitant fees, and misleading information. It’s essential to research lenders thoroughly, read reviews, and ensure they are reputable before applying for a loan.

How to Mitigate the Risks

Understanding the risks associated with instant approval loans is the first step in mitigating them. Here are some strategies to consider:

Shop Around for the Best Rates

Not all instant approval loans are created equal. Interest rates and fees can vary significantly between lenders. Take the time to compare different loan options and choose the one with the most favorable terms. Online comparison tools can be helpful in this regard.

Read the Fine Print

Always read the loan agreement carefully before signing. Ensure you understand the interest rate, repayment terms, fees, and any penalties for late or missed payments. If anything needs clarification, ask the lender to explain it to you.

Borrow Only What You Need

It can be tempting to borrow more than you need when a lender offers a more significant loan amount, but this can lead to higher interest costs and financial strain. Borrow only the amount you need to cover your immediate expenses and ensure you can repay it within the specified timeframe.

Have a Repayment Plan

Before taking out an instant approval loan, have a clear plan for how to repay it. Consider your income, other financial obligations, and the loan’s repayment schedule. If you need help determining whether you can repay the loan on time, it might be better to explore other options.

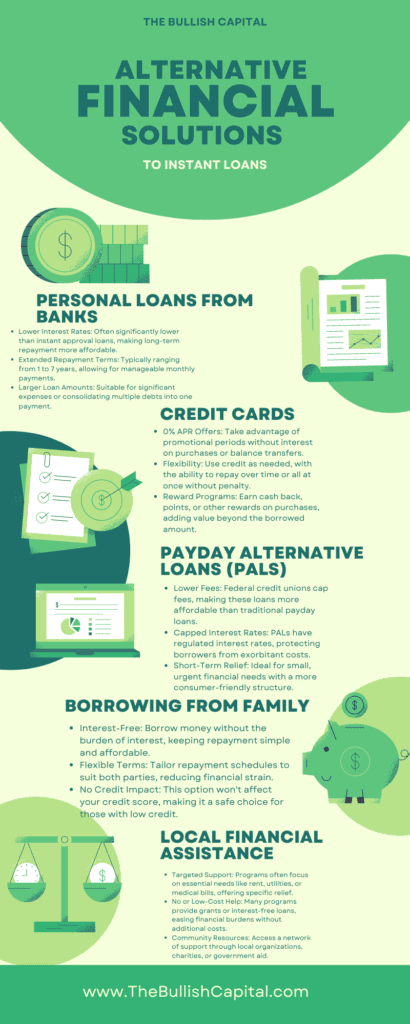

Consider These Alternatives to Instant Loans

Consider alternative options if the risks of instant approval loans seem too high. These include using a credit card, requesting an advance on your paycheck, or exploring personal loans with extended repayment periods and lower interest rates.

Instant approval loans offer several benefits, including quick access to cash and a simple application process. However, they also come with significant risks, such as high interest rates, short repayment terms, and the potential for falling into a cycle of debt. By carefully weighing the benefits and risks, shopping around for the best terms, and having a solid repayment plan, you can make a more informed decision about whether an instant approval loan is the right choice for your financial situation.

In the next section, we’ll explore some of the top instant approval loan providers, helping you compare your options and choose the lender that best meets your needs. Stay tuned as we continue to guide you through the world of instant approval loans, ensuring you have the knowledge and tools to make the best financial decisions.

LightStream® Personal Loans

Overall Rating: 4.5/5

Upstart® Personal Loans

Overall Rating: 4.2/5

Avant® Personal Loans

Overall Rating: 4.0/5

LendingPoint® Personal Loans

Overall Rating: 4.1/5

Upgrade® Personal Loans

Overall Rating: 4.3/5

Discover® Personal Loans

Overall Rating: 4.6/5

OneMain Financial® Personal Loans

Overall Rating: 3.8/5

Oportun® Personal Loans

Overall Rating: 3.7/5

SoFi® Personal Loans

Overall Rating: 4.7/5

RocketLoans® Personal Loans

Overall Rating: 4.0/5

Debt Financing vs. Equity Financing: What’s the Difference?

When it comes to funding your business, there are two...

Pros and Cons of Financing a Car: Is It the Right Choice for You?

When purchasing a vehicle, deciding how to pay for it...